Blog May 20, 2019

Blockchain is More Than Bitcoin

For many the word “Blockchain” conjures up word associations like Crypto Currencies, Dark Money, Bitcoin, Ethereum, and Mining. While Bitcoins and other crypto currencies are arguably the publicly best-known systems based on blockchain, it is worth having a look at blockchain itself and its potential applications.

The History

When did this all start? In the 1990’s Stuart Haber and W. Scott Stornetta, and joined by Dave Bayer soon after, worked on a system for archiving data in such way that it could not be tampered with after it was stored. They came up with a chain of data blocks that were secured by timestamps that could not be tampered with.

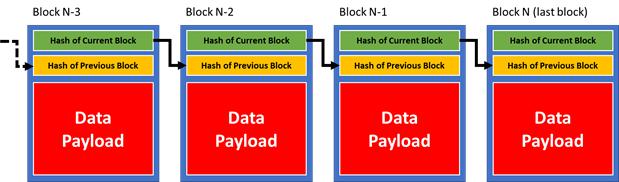

In 2008, Satoshi Nakamoto (interestingly enough, it is not known if this is a single person or a pseudonym for a group of persons – a fact that certainly contributes to the mystery blockchains and blockchain-based currencies are shrouded with) conceptualized a chain of data blocks that were secured by a cryptographic method called a “hash”. A hash is essentially a translation of data of arbitrary size into a unique, fixed length code. Nakamoto’s idea was to set up a chain of data blocks, where each block contains not only the data itself (the “payload”) but also the hash of the previous block.

So, What is it?

In essence, each block would implicitly inherit information about all preceding blocks in the chain. If someone was trying to change the data in an earlier block, all the succeeding blocks would have to be recalculated (specifically the hash). A good way to visualize this concept is to think about ourselves: Each of us carries the genetic traces of our entire family tree in us. In order to exist, all our parents and their parents, that is our entire family tree, must exist. If something would change in our family tree, we would not exist. This fact is frequently exploited in SciFi movies like the 1985 comedy “Back to the Future” in which main character Marty McFly changes the timeline of his prospective parents thus risking being “erased”. In “blockchain-speech”: If someone changes the data in a block, the entire subsequent chain must be recreated, and this new version including the last block will differ from the original chain.

How It's Secure

The system of securing the contents of all blocks in a chain by hash-inheritance alone does not make the chain tamper-proof. Using today’s fast computers, it would be possible to recalculate an entire chain almost instantly. Hence two more requirements are necessary: First, the entire chain of blocks must be visible and accessible to all who have a stake in the data contained in the blockchain. Typically, that means that the chain has no access restrictions. Each participant has a copy of the chain (or at least has the right to obtain a copy even if when choosing not to exercise this right) and can verify the validity of the chain by comparing their own copy to all others. There are also private blockchains where access is tightly controlled by a single entity, and so-called consortium blockchains, that are restricted-access only. For the later, access is controlled by a group of organizations, e.g. companies. However, usually, the blockchain is a “decentralized public ledger”. As a side-note, regardless of the accessibility status of the blockchain itself, the data payload could be encrypted and thus not accessible to prying eyes.

Secondly, as mentioned above powerful computers could quickly recalculate a counterfeited chain. Hence, constraints for the hashes were introduced that in effect slow down the hash calculation significantly. Because the blockchain is a public ledger that is expensive to (re)calculate, the longest chain must be the correct one: Only if I have more computing power available to me than all the other participants in the chain combined could I build a chain that is longer than all the other copies and thus create a forged chain. This is also known as a “51% attack”. However, in practice this is not a realistic scenario: I would either have to spend a lot of money (more than the other participants) thus diminishing the potential net profit I could gain from such an attack, or I would have to convince most of the other participants to tamper with the chain, which is not realistic either.

Now, hash calculation becoming a computational expensive, time-consuming activity, many commercial implementations based on blockchains such as Bitcoin reward participants for calculating hashes (a process also called “mining”): Whoever calculates a hash that conforms to the constraints for a new block first (thus “sealing” the block) is given a reward, for instance a fraction of a Bitcoin.

Cheat Sheet:

- Blockchain is a tamperproof system for storing any kind of data.

- The data is stored in blocks containing the data payload and a hash.

- Typically, the chain of blocks is public, each participant maintains a copy of the chain.

- Adding a new block to the chain is computationally expensive due to the constraints placed on calculating the hash.

- The longest chain “wins.”

- A chain can only be tampered with if the attacker commands more the rest of the total available computing power.

Now What?

Now that there is a system that stores data that cannot be modified once a data block is “sealed”, what can we do with it? In commercial and non-commercial interactions, often a “trusted authority” is needed to verify that validity and correctness of the information involved, and to keep records of the transactions. For instance, when buying a house, the seller and buyer exchange the legal documents and contracts, and the transaction is then recorded by a public registry, i.e. the Recorder of Deeds. Hence, if there is any question about the ownership of a certain property, one can simply make an inquiry to this public (trusted) registry and find out who the actual owner is.

Or, let’s think about banks: Both you and your employer have (implicitly) agreed that the bank is a “trusted authority” that will record the salary payment your employer makes to you each month. In case there is a dispute of whether your salary has been paid, you would first check your bank records and then talk to HR. They would also check their bank records, and thus be able to prove that they did pay you that month.

Now let’s imagine a situation you don’t want to use such a trusted “middleman” and deal with your business partner directly: What you and your business partner need is a system where both of you can record information (e.g. sales agreements, payment information, shipping confirmation, etc.) that cannot be tampered with after both you and your business partner submitted the information. Voilà! We just described the characteristics of a blockchain!

Real-world examples:

Cryptocurrencies such as Bitcoin employ blockchains to record the transfer of funds between different accounts without using the services of conventional “clearing houses” such as banks and credit card companies. All transactions are recorded in a blockchain. The transactions are visible to all Bitcoin clients and cannot be tampered with. Lately, “hacking of Bitcoin” made the news. It is important to note that those crimes did not tamper with the underlying blockchain itself but with the systems managing the transfer of funds. The blockchain itself was still intact but the attackers managed to direct funds to their own accounts. Using blockchain in finance is not limited to cryptocurrencies: Increasingly, “traditional” banks and other financial institutions such as brokerage firms employ blockchains to document and archive their transactions, too.

We already mentioned the transfer of property rights (through a sale or otherwise) as an opportunity to employ blockchain. In this use case, the records documenting the ownership transfer could be archived in a blockchain. For instance, if you buy a car, you and the car dealership could file the sales contract in a blockchain. In general, any contract could be stored in such system: For example, when you make a travel reservation or sign up for an insurance, the contracts and documents could be handled and archived by a blockchain. Likewise, instead of leaving one’s Last Will and Testament with a family member, a lawyer or another trusted person, one could simply store it in a blockchain-based depository.

In the commercial world, a shipping company could establish a chain of custody for all its shipping containers. Particularly in international shipping operations, shipping containers are usually handled (and transported) by several different entities, for instance by a trucking company from the origin to a port, by freighter to another port, and then again by a trucking company to the destination. At each hand-over, documents such as the transportation contracts, bill of lading, and customs declarations must change hands, too. If any of those documents are missing or wrong, or if there is doubt about the validity and correctness of those documents, expensive delays can occur. By using a blockchain-based system, the custody of each shipping container and the associated shipping documents become ubiquitous to all parties involved. A 3rd party trusted by all is not required anymore.

Another field of application for blockchains is healthcare: The possibility of “hacking” an Electronic Medical Record (EMR) and manipulating the medical information to the detriment of the patient is cause for serious concerns. The immutability of information stored in blockchains could alleviate this problem or eliminate it entirely.

One last example: With the Internet of Things (IoT) starting to permeate daily life, it becomes increasingly important that have tamper-proof registries of each IoT device in order to prevent attacks on the IoT network (e.g. through spoofing the identity of a specific device or group of devices.) A blockchain-based registry could solve this problem.

Conclusion

There are many other areas where blockchain could help. But if they are so versatile, why have blockchains not yet permeated many more business or personal areas? One reason seems to be scalability: In particular, for blockchains with many participants (such as the cryptocurrencies mentioned above), the constraints imposed on the hash make the computation increasingly slow, energy consuming and expensive. This means that blockchains can be slow to process transactions: On average, the Bitcoin-system can process about 10 transactions/second. By comparison, in the US alone the credit card company VISA can process over 25,000 transactions/second. Further, all those hash-mining calculations can consume a log of electric energy. It has been estimated that in 2018 the global energy consumption for mining Bitcoins exceeded the energy consumption of Iceland! Thus, blockchains seem to be suited best for systems that require only low to medium transaction speeds and don’t have a too large number of participants to keep the mining costs under control.Even taking into account the limitations mentioned above, blockchains can be a powerful instrument and are solving real-world problems today.